by Rachel Gore

Inflation. It’s a word most are familiar with and is used in news headlines every day. Inflation has reached new heights since the pandemic started. Even those who do not watch the news can’t avoid it. Inflation affects every American’s everyday life, whether they’re wincing at gas prices or switching to a cheaper brand at the grocery store. But the true cost of inflation is a lot more complex than expensive gas.

The Basics of Inflation

Inflation is a price increase in goods and services and a corresponding loss in purchasing power. Simply put, high inflation means money does not go as far as it used to. If you walk into the store with $100, you will be walking out with less to show for it than you would have when inflation was lower.

The federal reserve measures inflation by changes in a price index, which is a measure of relative price changes. The Consumer Price Index and Personal Consumption Expenditures Index are the most frequently used price indexes in the United States. Both indexes measure inflation based on the average price change of a basket of goods and services. While the Consumer Price Index focuses exclusively on urban consumers, the Personal Consumption Index considers all households.

To put this into perspective, consider a gallon of milk. The Consumer Price Index indicates that the average price for a gallon of milk increased from $3.92 to $4.01 between Marchand April 2022. That’s a 2.4% increase. While that may seem insignificant, these increases add up over time. In 1995, milk averaged just $2.48 per gallon. Plus, when nearly every item in the grocery store and other essentials follow a similar upward trajectory, that’s a lot more spending each year.

Is Inflation A Bad Thing?

Inflation is not inherently bad. When rising inflation coincides with increased wages, consumers can benefit. Think of a student loan borrower who took out $50,000 in loans in 2010. Thanks to inflation, they can now pay that loan back with money worth less than when they initially borrowed it. That’s because $50,000 in2010 equals around $66,000 in purchasing power in 2022.

Problems arise when inflation rises too quickly. While the Federal Reserve doesn’t have a formal inflation target, its website suggests that a moderate inflation rate of around 2% is the sweet spot. While well-off households may be able to shoulder high inflation by cutting down on discretionary spending, those who live paycheck-to-paycheck may struggle to pay for necessities like food and shelter.

High inflation is also detrimental to the stock market because investors must make higher returns on their investments to breakeven in terms of purchasing power. High inflation can also cause small business profit margins to take a hit if businesses are forced to absorb the cost of the increase.

The State of Inflation in 2022

The Consumer Price Index rose 8.5% between March 2021and March 2022, meaning the same necessities that cost $100in March 2021 now costs $108.50 in 2022. Inflation has not been that high in the United States since 1981. Meanwhile, the Personal Consumption Expenditures Index rose 6.4%, the highest rise since 1982. The message is clear between the two indexes: consumers pay a lot more for household goods and services than they used to.

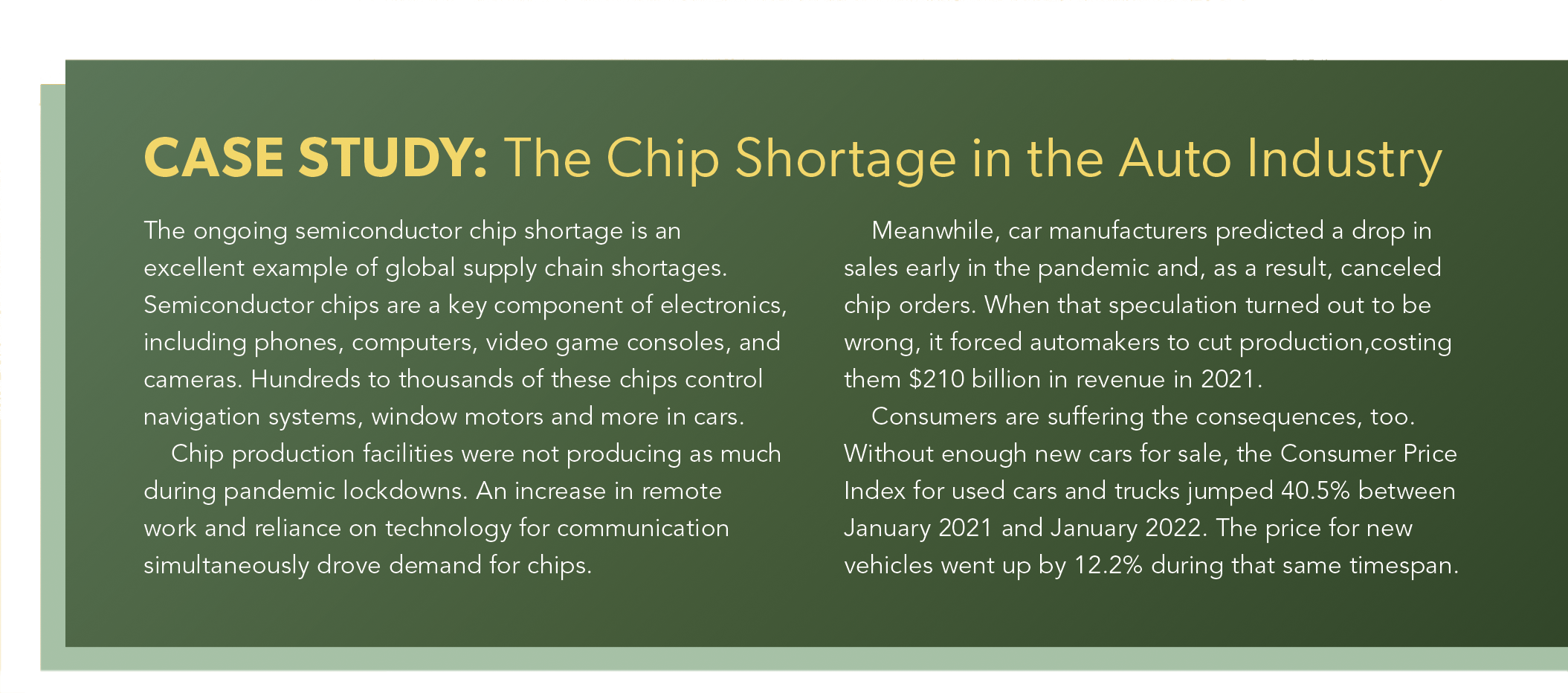

There are a few factors that led us to where we are today. Consumer spending and supply and demand contributed to the problem, but some extenuating circumstances caused this record-setting spike.

Extenuating Circumstances

When the pandemic emerged in early 2020, the global economy halted abruptly. Consumers bunkered down in their homes to stay safe from the virus. Restaurants stopped serving their patrons in person or closed their doors for good. Retailers shuttered their doors and shifted to e-commerce business models. Companies laid off 114 million workers globally to cut costs. Demand for goods and services dropped drastically.

During this time, the Federal Reserve worked hard to keep the economy afloat. It dramatically cut interest rates and absorbed corporate debt. Multiple stimulus packages flooded the economy with stimulus checks, unemployment assistance and small business aid.

President Biden’s $1.9 trillion stimulus relief bill left many Americans with more money in their pockets by the summer of 2020. Demand skyrocketed as a result, but shipping delays and material and labor shortages meant that supply could not keep up. High demand, low supply and production delays led to further inflation. Panic-fueled stockpiling of goods exasperated supply chain issues even more. Two years into the pandemic, supply chain problems remain. Although most Americans are eager to return “back to normal, “the economy simply isn’t there yet.

On February 24, 2022, Russia launched its large-scale invasion of Ukraine. The resulting war between the two countries is contributing to rising inflation.

The Ukraine-Russia region is one of the world’s global major food suppliers. The area is a vital exporter of wheat, sunflower, fertilizer and oil. In fact, it supplies 30% of global wheat exports and 65% of global sunflower exports.

The United States sanctioned and banned oil, gas and coal imports from Russia due to the invasions. The trade interference has enormous implications because the U.S. gets around 20%of its petroleum products from Russia. It’s not alone. Many other countries, particularly those in Europe, get an even higher percentage of their petroleum products from Russia. Being cutoff from one of the biggest oil producers in the world led to a price hike in crude oil. One barrel of crude oil cost over $110 in May 2022, up from less than $80 in early January.The most visible impact of this is the rising gas prices. The average cost for a gallon of regular gas was $4.59 on May 22, 2022. All 50 states now have an average of over $4 per gallon. On December 20, 2021, before the invasion began, the national average was $3.31.

The United States sanctioned and banned oil, gas and coal imports from Russia due to the invasions. The trade interference has enormous implications because the U.S. gets around 20%of its petroleum products from Russia. It’s not alone. Many other countries, particularly those in Europe, get an even higher percentage of their petroleum products from Russia. Being cutoff from one of the biggest oil producers in the world led to a price hike in crude oil. One barrel of crude oil cost over $110 in May 2022, up from less than $80 in early January.The most visible impact of this is the rising gas prices. The average cost for a gallon of regular gas was $4.59 on May 22, 2022. All 50 states now have an average of over $4 per gallon. On December 20, 2021, before the invasion began, the national average was $3.31.

American consumers use 369 million gallons of motor gasoline a day. That means that Americans pay $369 million more per day each time gas prices increase by $1. With no end in sight for the war and a mixed bag of predictions on when prices could go down, Americans will likely be spending more on gas for some time.

The True Cost of Inflation: Housing

Inflation has also severely impacted housing costs in recent years. Inventory for homes is scarce compared to demand, triggering raging bidding wars and sales well above the homes’ asking price.

High mortgage interest rates are pushing some would-be homebuyers out of the market altogether. A 30-year fixed mortgage rate in May 2022 averaged 5.48%, compared to just 3.73% at the end of January. This difference can translate to hundreds of dollars more in housing costs per month. The result is that 30-year mortgages now cost 31% of the median American household’s income–the largest share since 2007.

Renters are not faring much better. Redfin found that the average monthly rent was $1877 in December 2021, a 14%year-over-year increase. The 10 metro areas with the fastest rising rental rates all saw 29% or more increases. Fortunately, it’s not all bad news. Redfin also found that homebuyer demand is beginning to slip. On top of that, the share of home sellers reducing their asking price is ticking upward. Even so, housing prices have jumped significantly in the past year. Even if that growth slows, the next year will likely bring even higher price tag.

The True Cost of Inflation: Food

The cost of food is rising, too. The CPI found that food item prices increased 8.8% in the year ending in March 2022. Flour, butter, meat, milk, eggs, fruit, bread, vegetables and other household staples increased in price. Altogether, food prepared at home costs around 10% more in early 2022 than in 2021. In comparison, takeout and restaurant meals have risen by 6.9%.

Supply chain issues and rising labor costs caused much of this increase. The war in Ukraine has caused further upheaval in the food supply chain. With fewer goods being exported globally, price hikes and supply shortages have already begun.

The U.S. baby formula shortage highlights how dire situations can become when there is not enough food to go around. Milk powder, an essential ingredient in baby powder, was one of the items affected by supply shortages when the pandemic emerged. By January 2022, milk powder shortages were worsening significantly in the U.S. With substitutes to formula challenging to find, new parents began stockpiling their reserves.

The Abbott Nutrition baby formula recall compounded the issue. By late April 2022, nearly 40% of baby formula brands were sold-out nationwide. The shortage has left several babies hospitalized. While inflation is not the only contributing factor to this shortage, it has not made things easier.

When Will Efforts to Reduce Inflation Pay Off?

In early May 2022, the Federal Reserve raised its key interest rate range to 0.75% –1%. Before that increase, the rate was at 0.25–0.5%. The increase was the largest one since 2000.

Higher interest rates can decrease inflation by reducing consumer spending—when goods and services cost more, people spend less. With a decrease in demand for goods and services, inflation should fall.

In a Wall Street Journal live stream on May 17, 2022, Federal Reserve Chair Jerome Powell noted that further action is likely.” What we need to see is clear and convincing evidence that inflation pressures are abating and inflation is coming down—and if we don’t see that, then we’ll have to consider moving more aggressively. If we do see that, then we can consider moving to a slower pace,” he said.

What will happen next? Only time will tell. Some estimates indicate that interest rates could peak at 3.5%, which is over three times higher than it is today. Others anticipate more moderate gains. There are also predictions that this approach to inflation control will lead to a recession.

All in all, it’s impossible to know for sure what the future holds. In the meantime, consumers will need to tread carefully when it comes to spending to reduce the high cost of inflation in their lives.

Leave A Comment